Debate

Is DeFi Paying Lenders Enough?

If you’re depositing USDC into a Morpho vault for 3-4% APY, you might be getting fleeced.

That’s the argument from Luca Prosperi, founder of M0 and author of the Dirt Roads newsletter. He just dropped the first part of a three-part series applying Wall Street-grade math to onchain lending.

His conclusion: DeFi lenders are drastically undercompensated for the risk they’re taking.

His piece gets very technical. I’ll simplify the core argument here, but if you want the full quant breakdown, the original article is worth your time.

So what did he find? Luca splits Morpho activity into three buckets:

1. Overcollateralized lending on liquid crypto collateral. This is Morpho’s bread and butter. You deposit USDC, and someone borrows against their ETH. Simple.

2. Leverage looping. Deposit wstETH, borrow ETH, loop it. We’ve covered this before. Luca models these as basis trades, and they work well when spreads are stable.

3. RWA-based lending. Non-crypto collateral, like private credit. Luca is bearish here because RWA collateral is inferior to crypto-native assets: it’s illiquid, price feeds are stale, and liquidation takes weeks instead of seconds.

(There are niche protocols like 3F trying to add crypto-like properties to RWA collateral. But they’re not live yet.)

The spicy take is on bucket #1.

The put option you didn’t know you sold

Luca models depositing USDC into a Morpho vault backed by ETH as two things happening at once: you’re holding a risk-free bond, and you’re selling a put option on that ETH collateral. The liquidation loan-to-value (LLTV) acts as the strike price.

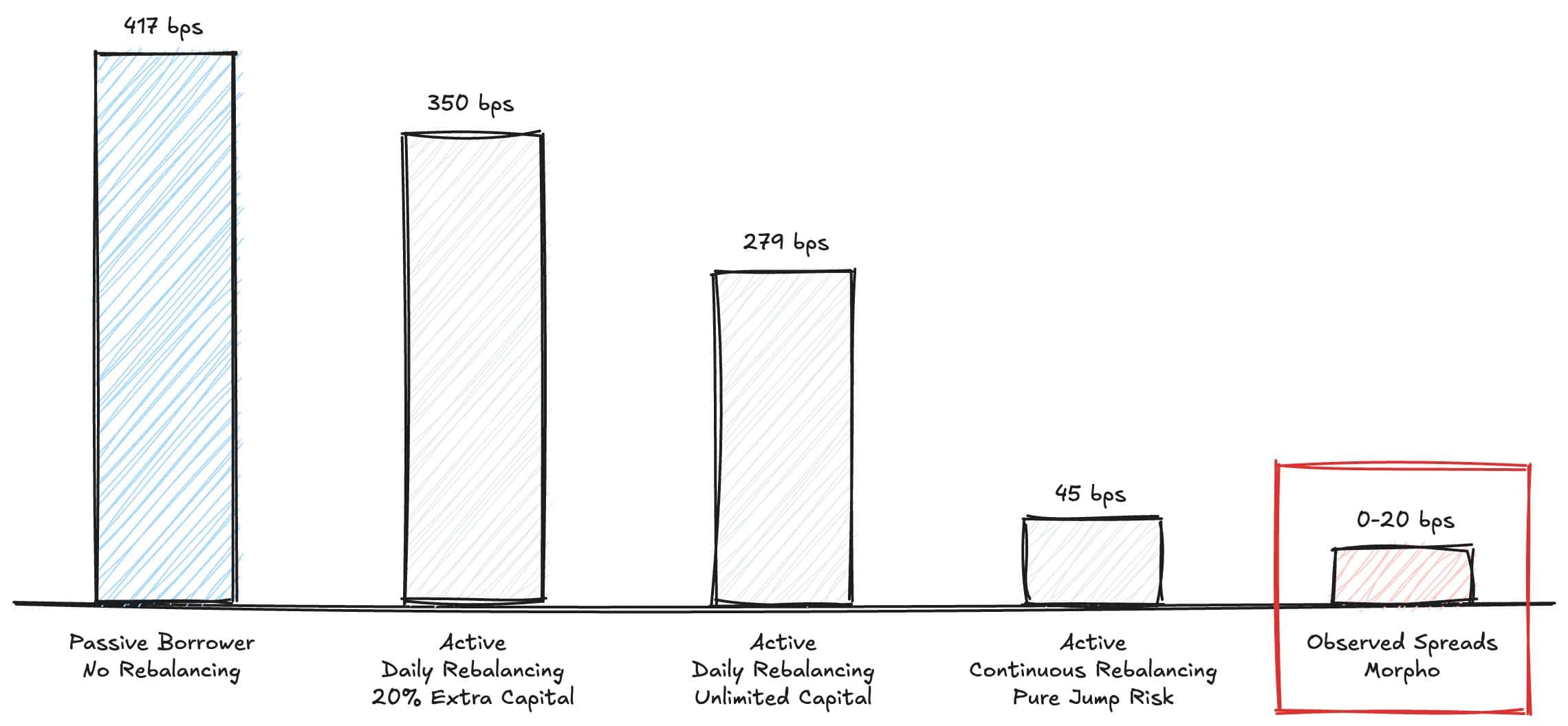

Using a first-passage credit model (Black-Cox framework), he calculates what lenders should be earning for this risk. The numbers:

- Floor: 45 bps (0.45%) above the risk-free rate, assuming borrowers have unlimited capital to top up collateral. Best case scenario.

- Realistic range: 250-400 bps (2.5-4%) above risk-free, assuming normal borrower behavior.

The current risk-free rate (SOFR) sits at 3.65%. So lenders should be getting at minimum ~4.1% APY, and realistically 6.15-7.65%.

Morpho depositors are earning 2-4% APY.

That’s a big gap.

Why are lenders accepting this?

Luca points to a few reasons:

- Regulation (the GENIUS Act) prevents stablecoin issuers from sharing yield directly. So onchain investors can’t actually access the risk-free yield.

- Depositor misperception. Retail users routed through Coinbase and similar UIs think they’re in a savings product, not a credit product.

- Survivorship bias. No major blowup has hit the flagship vaults yet, so the risk feels abstract.

- Bull markets make everything look safe because collateral doesn’t get liquidated.

- Token incentives made lenders accept lower base APY.

Not everyone agrees with Luca tho. Crypto Twitter had good counters.

Adrian (@adcv_) from Steakhouse, one of Morpho’s top vault curators, argued that on-chain lending is structurally closer to a repurchase agreement (repo) than a put option sale.

This matters because it changes a key input in Luca’s model: loss-given-default (LGD). Luca uses ~5% (the liquidation incentive). Adrian argues the actual empirical bad debt rate for prime vaults is closer to a few basis points. Plug that number in, and the model’s predicted rates match what Morpho is actually paying. The “mispricing” disappears.

Sam from Spark made a different case: the real risks in on-chain lending are fundamental (custody failures, oracle bugs, smart contract risk), not market price jumps.

And crypto-native actors rationally accept lower yields because on-chain capital has a liquidity premium. If you’re a hedge fund and you need to deploy capital in minutes, waiting for a TradFi wire transfer could cost you more than the yield difference. Being onchain is worth something.

What to make of all this?

The debate is genuinely great. DeFi needs more of this: rigorous, quantitative thinking applied to products that manage billions of dollars.

Whether Luca’s model perfectly captures reality or not, the core question matters. Do you actually understand the risk you’re taking when you deposit into a lending vault?

If you want to go deeper:

Sponsored by Stacks

Stacks: The Bitcoin L2 Grow Your BTC Stack

Most Bitcoiners just HODL like a dragon sitting on gold. The problem? That BTC stack isn’t doing anything for you.

Stacks, the leading Bitcoin L2, wants to change that.

They’ve launched a virtual series called “Growing Bitcoin” exploring ways to make BTC a productive asset. The centerpiece: Dual Stacking.

How it works:

sBTC is a 1:1 BTC-backed wrapper you can use across DeFi and dApps on Stacks.

- Just holding sBTC earns you ~0.5% yield passively.

- Stake STX alongside your sBTC, and that jumps to ~3–5%+ depending on the ratio. That’s Dual Stacking.

- Last week, we covered an adjacent strategy: earning BTC by stacking STX. No other BTC-denominated yield creates such a high yield (~10%) with consistency.

They also have a self-custodial BTC staking product coming. But that’s a topic for later.

Where does the yield come from?

Stacks’ consensus mechanism, Proof-of-Transfer. Not some mystery box of rehypothecated risk. The yield source is transparent and baked into the protocol.

The kicker: sBTC stays liquid. You can deploy it across the Stacks ecosystem for additional yield on top.

Denominate in BTC. Earn in BTC. Keep your stack growing.

Subtopic

Polymarket’s Biggest Update Ever

Polymarket just announced the biggest overhaul in its history.

New trading engine. New collateral token. New order book. All rolling out over the next 2-3 weeks.

What’s happening? Polymarket is shipping many major upgrades at once, and the timing isn’t random. Intercontinental Exchange (the company that owns the NYSE) just invested $600M into Polymarket, with up to $2B committed.

The platform is evolving from a retail prediction market into a full-blown professional trading venue built for institutional participants, bots, and brokers.

Here’s what’s changing:

1. Rebuilt Trading Engine

The entire order book and matching engine are getting replaced. The new system settles trades faster, cuts gas costs, and supports EIP-1271 — an Ethereum standard that lets smart contract wallets (multisigs, automated trading bots) sign transactions natively.

That last part matters. Professional trading desks run on bots, APIs, and multi-sig wallets. Without EIP-1271 support, Polymarket was basically asking institutional players to use consumer-grade infrastructure. Not anymore.

2. Polymarket USD

Polymarket is ditching USDC.e (a bridged version of USDC on Polygon) and replacing it with its own token: Polymarket USD, backed 1:1 by Circle’s USDC.

(It’s a stablecoin, but they aren’t using that term anywhere, probably for legal reasons.)

Two reasons Polymarket USD makes sense.

First, bridge risk. USDC.e relies on a bridge to move USDC onto Polygon. Bridges have been one of crypto’s biggest attack vectors. Removing that dependency is a straightforward security win.

Second — and this is speculation — Polymarket could be positioning itself to earn revenue from Circle.

We’ve talked about the custom stablecoin trend multiple times in this newsletter. Protocols that drive demand for USDC tokens can negotiate revenue-sharing deals with Circle. Coinbase and Lighter already do this.

Open Interest on Polymarket? That’s leverage that can be monetised.

For most users, the frontend handles the conversion automatically with a one-time approval prompt. Power users and bot operators will need to manually wrap their USDC or USDC.e into Polymarket USD via a smart contract function.

3. Builder Codes for Onchain Attribution

Think of these as onchain referral links. Third-party builders, affiliates, and integrators can now get attribution for the volume they drive to Polymarket.

It’s a small addition, but it opens the door for a proper distribution layer on top of the platform.

Imagine sports influencers shilling prediction markets around game outcomes, or political commentators embedding markets into their content. That’s potentially a big growth vector for Polymarket.

What about a POLY token?

Nothing. Zero mention in the announcement.

If you’ve been farming Polymarket hoping for an airdrop, this isn’t the update you were waiting for. The platform just shipped a custom stablecoin, a new trading engine, and an attribution system — and still no token in sight. Read into that however you want.

What you need to know

During the migration, all existing order books will be cleared. Polymarket says they’ll give at least one week’s notice before the maintenance window.

If you have open positions or active orders, keep an eye on their announcements. Your open orders will be cancelled during the migration.

The full migration guide and API changelog haven’t dropped yet, so we’re working with limited information.

I’ve kept this high-level on purpose. If you’re a builder or bot operator, the full announcement has more details that you’ll need.

🚀 DeFi Catalysts

Aave lost Chaos Labs as a risk provider. Aave cited unreasonable demands (like exclusivity & vendor lock-in) as the cause for the split.

YieldCompass is a standardised, open-source framework to compare risk and realised returns across DeFi opportunities on Solana.

Morpho introduced the Beta of Morpho Agents. It’s an interface that’ll allow agents to read, simulate, and write to Morpho protocols.

Polymarket is upgrading its entire stack over the next 2-3 weeks. It’ll also introduce Polymarket USD, backed 1:1 by USDC.

Pendle launched Limit Order (LO) Incentives across all Pendle pools. In-range orders will receive up to 100% APR.

Sushi Perps went live. It is powered by HyperLiquid. The early traders will get boosted Sushi point multipliers.

Solana Foundation launched Solana Agent Skills. They are pre-built skills you can drop into AI tools to interact with Solana.

Ethena released an article on the backing of USDe. It has moved away from mostly perp-short basis trades into a mix of strategies.

Alchemix, the protocol offering self-repaying, interest-free, and non-liquidating loans, has frozen its v2 and is moving all positions to v3.

Midas introduced mROX. It’s a new onchain investment product built with RockawayX, a $2B AUM digital asset firm.

Drift Protocol revealed more details of its hack. It involved a fake “quant fund” spent 6+ months befriending the team IRL and deposited $1M.

📰 Industry News

Fox News has integrated Kalshi to be used in news broadcasts. Kalshi said sports may be included in the future.

Circle is launching its BTC Wrapper. It’ll be called crcBTC and backed 1:1 by BTC. The backing will be verifiable onchain as well.

Solana Foundation launched STRIDE and SIRN to boost the Solana ecosystem security. Solana’s biggest DeFi hack happened last week.

Biconomy and the Ethereum Foundation released ERC-8211, the execution standard for onchain agents.

FDIC approved a proposed rule to implement the GENIUS Act, the stablecoin legislation. It establishes a framework for stablecoin issuers.

🐦⬛ X Hits

- Is STRC the next UST?

- Why Crypto will be back.

- Ray Dalio on the US-Iran war.

- Why HIP-4 will take over finance?

- Deep dive on launchpads with focus on MetaDAO.

😂 Meme

Until next time,

Edgy

Today’s email was written by Edgy and Yayya.

DISCLAIMER: I’m NOT a financial advisor. This content is for education and information purposes only. Crypto and DeFi are risky and speculative. Please do your research before investing.

|

|

|

Be Early to the Next Opportunities

TDE Pro gives you direct access to our research, our portfolios, and the gems we’re betting on.

It’s your unfair advantage to move before the crowds.

|

Whenever you’re ready, here’s how we can help you:

- ⚙️ The DeFi Edge PRO – Designed for busy people who want to stay ahead of the curve. Leverage our research to save you hours each week, and to see what we’re personally investing in. Join today.

- 🚀 The DeFi Edge Ventures – We identify, invest, and help amplify DeFi Protocols that positively impact the Crypto space.

You’re receiving this email because you signed up for my newsletter. You can update your Preferences or Unsubscribe here.

600 1st Ave, Ste 330 PMB 92768, Seattle, WA 98104-2246