The DeFi Quarter 3 Rewind: RWAs, Bots, and Trading Your Friends

Up, down, up, down – the amount of choppiness we’ve seen can drive a trader crazy.

On-chain activity this quarter has been some of the lowest we’ve seen since the bear market started.

This is a new series from The DeFi Edge where we’ll review each Quarter.

Lets look at some Stats from this quarter:

- DeFi TVL fell from 77 billion to 69 billion (~10.38%).

- The stablecoin MC also fell to $123B from $128B (~3.5%).

- $BTC decreased by 14% ($25k), and $ETH by 19% ($1,530).

- The total crypto market cap fell by around 9% to $1.119 trillion.

There were some bright spots despite the overall activity going down.

The Top 3 Narratives This Quarter

Some are old, and some are completely brand new. Here are some of the narratives that crushed it this quarter.

#1 Real World Assets

Investing in DeFi comes with risks such as exploits. It makes sense to take on the risk if the reward is worth it.

One metric we track is the median DeFi APY in DeFi. It has dropped to below 2%.

Contrast this with the treasury yield, the safest yield on the US dollar. The 3-month T-Bill rate is >5%. One of the primary reasons DeFi TVL is quite low is that the risk vs. reward ratio isn’t there.

If the yield stays low, capital will keep leaving DeFi. We need new sources of yield outside of printing tokens.

Enter Real World Assets…

RWAs bring traditional assets to the blockchain by tokenizing them. While all the graphs in DeFi are trending down, the graphs of RWA have been going up. And this could serve as a new source of yield for the space.

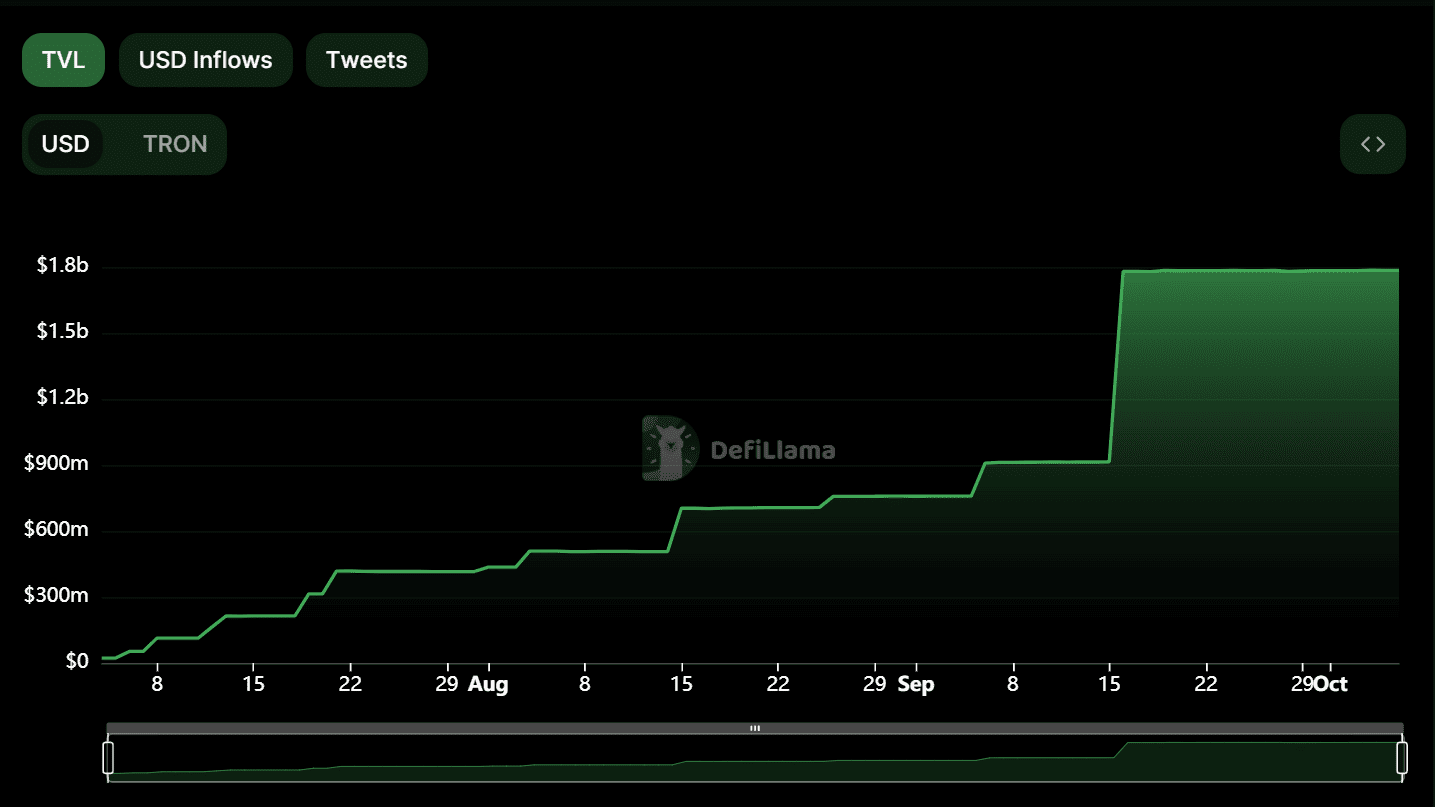

All the top 9 protocols in the RWA category are showing green on the 1-month TVL change. Top protocols like stUSDT and Ondo have been showing massive growth.

Here’s the TVL chart of stUSDT protocol.

Theoretically, we can tokenize a wide range of assets. From precious metals to real estate. But, the best asset to bring on-chain is the US T-bills.

MakerDAO took the lead in bringing treasury yield on-chain. They’ll lend DAI to groups who’ll invest in T-bills. The yield from T-bills is channeled onchain through interest payments on the DAI loan.

And the results are visible. In Q3, MKR price has rose from $830 to $1,530. For a dinosaur coin in a bear market, that’s really impressive.

Now other protocols are also following suit. Frax has set up a non-profit for handling US T-bills and other RWA stuff. Pendle tapped into the narrative by creating fUSDC & sDAI markets.

We wrote about Real World Assets back in March and we’re glad to see it growing.

#2 SocialFi

Tokenizing influencer accounts? Didn’t we already try this with Bitclout back in 2021?

Regardless, this new sector provided much-needed activity and interest in this dull market. This has been the surprise narrative of Quarter 3.

Leading the way is Friend.tech.

Friend.Tech 101: It allows anyone to issue “keys.” These keys can be traded. And the holders can access a private group chat with the key issuer. The theory is you’ll get exclusive alpha from the guys.

It instantly became a hit. Here are some numbers. Within its first month,

- ~138k unique users.

- ~3.4 million cumulative transactions.

- Cumulative protocol fees were $6.18 million USD.

Here are a few reasons for it going viral.

- Potential airdrop.

- A mobile application.

- Entertaining social game.

- A money-making opportunity.

- An ecosystem of apps is built on top of FT.

Once the narrative became popular, competitors emerged. New SocialFi protocols on different chains started popping up. Post.tech on Arbitrum, FanTech on Mantle, StarsArena on Avalance, and so on.

Here’s a chart showing the share of active subjects for different SocialFi protocols.

It tells the story of FT starting the narrative and competitors entering the market. Even though Friend3 is visible in the chart, Friend.tech dominated the market. Then came Post.tech on Arbitrum. It captured a significant share of the total users (~20% on Oct 5th).

Stars Arena (rebranded from Star Shares) was the latest major challenger. They captured a large percentage of users. But they had unverified contracts and were hacked. Now they’re out of the picture since no one is going to deposit money into their app anymore.

Also, regarding protocol fees and volume, Friend.tech is still the king. On Oct 5th, 91.6% of protocol fees and 82.2% of USD volume was with FT.

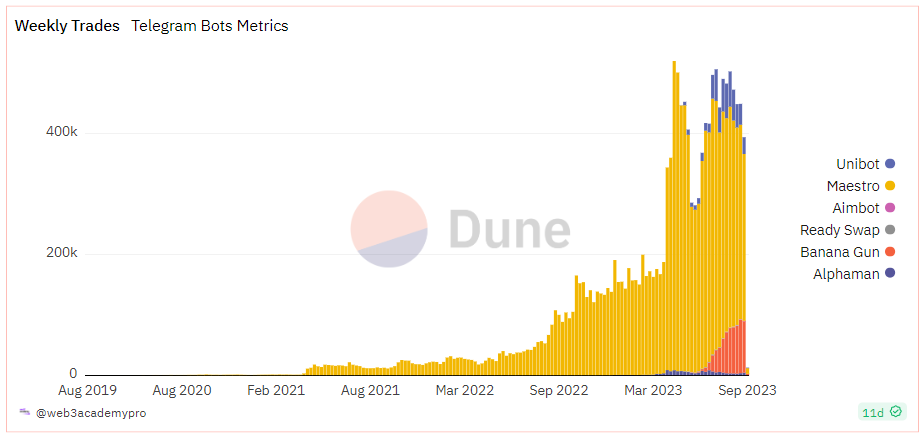

#3 Telegram Bots

I had noticed the massive fees they were printing and covered this narrative in my newsletter before it popped.

What are they? They are bots that allow users to trade crypto tokens from the telegram interface. And these bots aren’t just capable of basic buying and selling – they can also perform advanced tasks, including:

- Copy-trading.

- Handling airdrops.

- Portfolio management.

- Strategies, technical indicators, and more

This is a narrative with a lot of potential.

Bad UI/UX is one of the biggest problems in DeFi. Navigating the normal wallet + DEXes route is highly complex for beginners. Often, users have to jump between multiple websites, ensure security, approve all sorts of transactions, etc.

TG bots remove the need for that. They consolidate (almost) all activities into a familiar interface of Telegram. Bonus benefit: bots can be used from mobile phones as well, which isn’t common in the standard setup.

Telegram is a gigantic platform with over 550 million monthly active users, of which more than 55 million are daily active users.

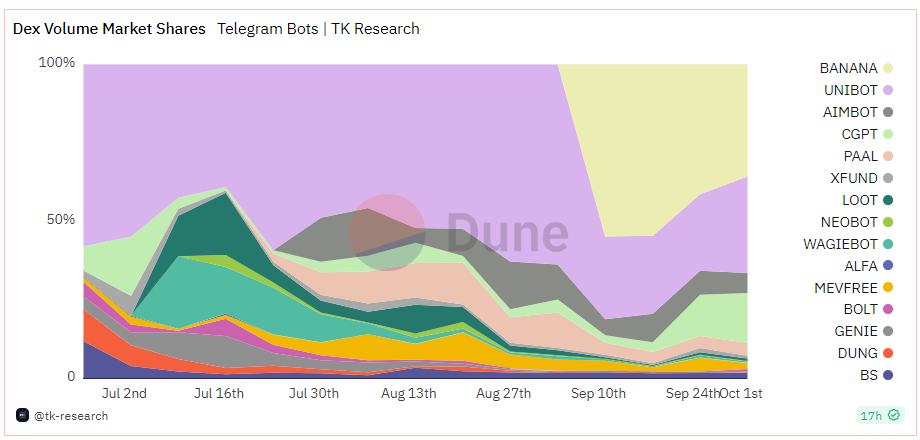

There are a lot of projects competing in this space. The following chart tracks the DEX volume market shares of different telegram bots.

Below are three projects in this narrative worth tracking.

#1 Maestro is the OG bot. In Q3, they had a revenue of $11.38 million. It still has around 70-ish (September data) percent of weekly trades in this category. However, they don’t have a token. If they launch a token, it’ll be massive.

#2 Unibot is the market leader (since Maestro doesn’t have a token). They share revenue with $UNIBOT token holders. Cumulatively, the holders have received more than $1.2 million in revenue.

#3 Banana Gun is the leading beta play. It is a comparatively new protocol. But if we exclude Maestro, they control ~35% of DEX volume market share. That’s more than Unibot. (They became infamous for failed token launch as well.)

Honorary mentions: LSDfi & GambleFi

To know more about LSDfi, read our deep dive on it. RollBit, a crypto casino, was leading the GambleFi narrative.

Top 3 Projects

These are the top three projects of Q3 that I felt were significant.

#1 Base

The Base chain officially launched on August 9th.

It is an Ethereum L2 powered by OP Stack. And it became an instant success. Here are some reasons.

- Backed by Coinbase.

- The Layer 2 rotation game.

- “Onchain summer” campaign.

- Friend.tech as a super app.

- Ecosystem fund to attract projects.

Despite being only 2 months old, it’s already 3rd largest Ethereum rollup by Total Value locked.

They also have a rich ecosystem of protocols. It already has 133 protocols. L2s launched around the same period, Mantle & Linea, only have around 30-ish protocols. Even Optimism, one of OG L2s, only has 190 protocols.

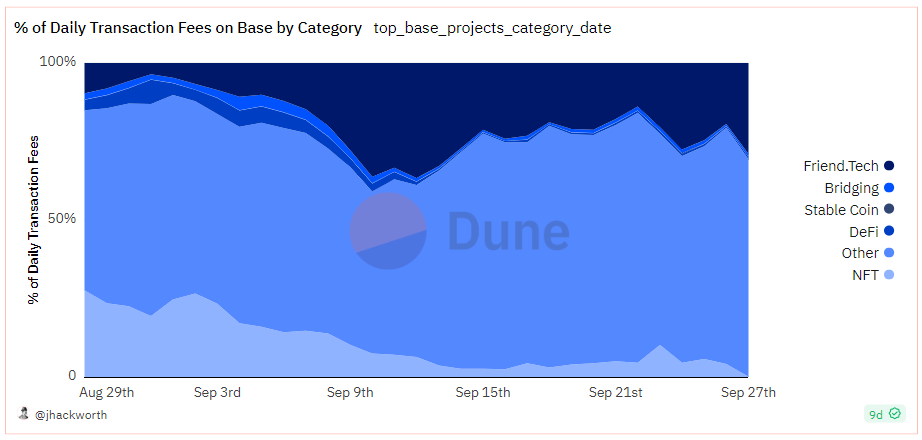

Base did really well in Q3. And all metrics are looking green. But for Q4, there are two headwinds:

- Arbitrum will start its Short-Term Incentive Program. This will pull liquidity away from Base into Arbitrum.

- Over-reliance on Friend.tech. On Sept 9th, 36.2% of daily transaction fees on Base were from Friend.tech. WTH! Is this an appchain or what?

#2 EigenLayer

It is a restaking protocol.

Restaking means taking staked Ethereum and re-staking it on some other protocol. You can restake your Liquid Staking Token as well as natively staked ETH.

And EigenLayer is a market between protocols and restakers. Protocols need actors to provide some service. And restakers will do that in return for yield. If they fail to do what they promised to do, they will lose their restaked ETH.

Another way to understand it is as a “Custom carrot & stick generator” for protocols. If the user behaves in the way the protocol wants, it’ll get carrots, aka the yield. If they don’t, EL will use the stick, aka slash the restaked ETH.

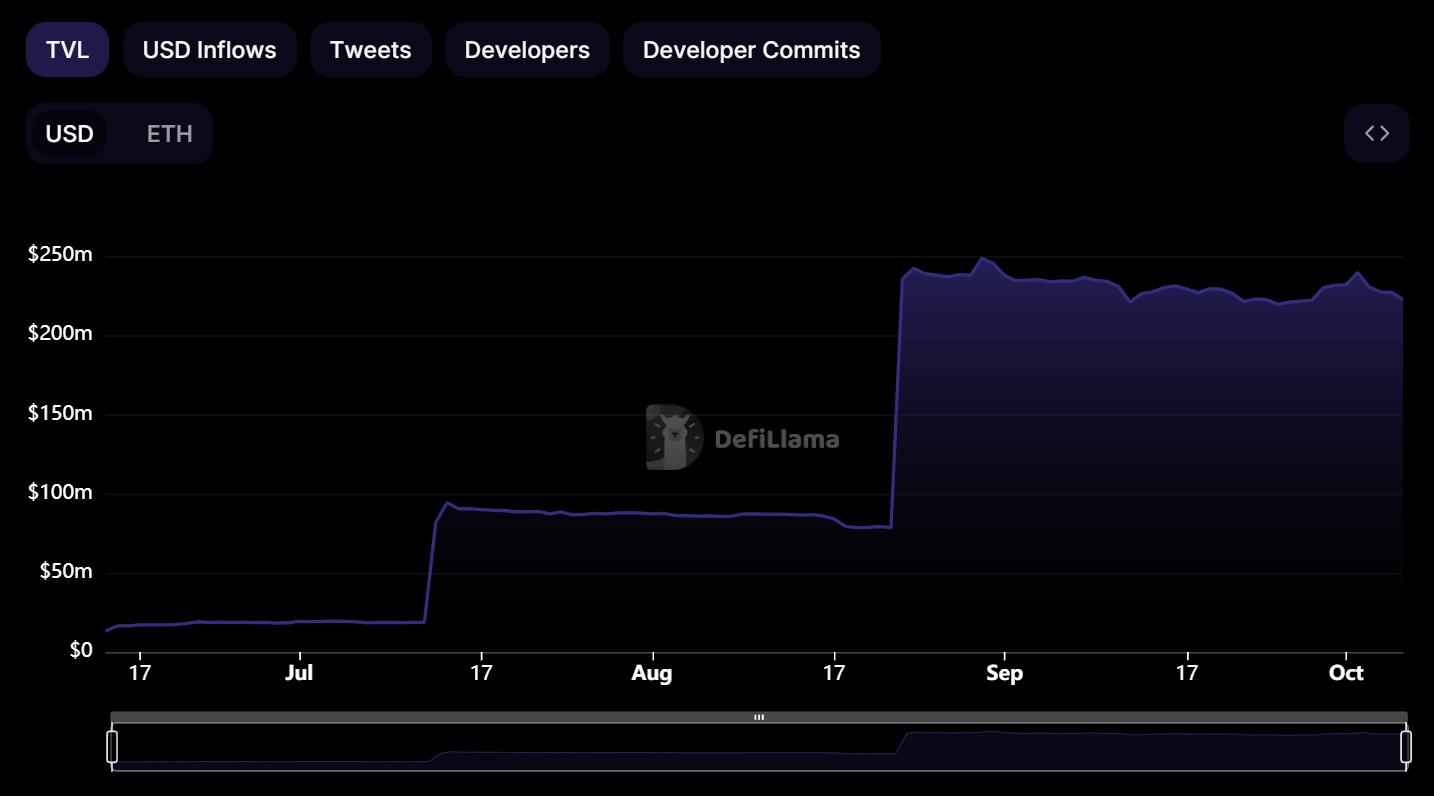

Their Ethereum mainnet launch was on June 14, 2023. For security reasons, they launched with restaking limits. It reached its maximum capacity on the launch day itself.

They increased the limit again on August 22, 2023. The cap for LSTs, including stETH, rETH, and cbETH, was lifted until any LSTs hit 100k tokens restaked.

This limit was also reached within hours. And the TVL rose from $78 million to $238 million. To put that in perspective, only 3 rollups have more TVL than that (according to DeFiLlama).

This shows the insane demand the EigenLayer has. As long as they manage to provide a functional product, it’ll be up only.

EigenLayer will enable new tokenomics mechanisms. Projects now have a new mechanism to distribute tokens in return for specific services.

It’ll also increase the rate of actual innovation. Previously, many decentralized projects were forced to create their own token networks. Projects can now outsource it to EigenLayer and focus on actual innovation. Twelve projects have already publicly started building on top of it.

Liquid Restaked Token is another innovation. They are kinda like Liquid Staking Tokens like stETH & rETH. Plus, they’ll capture the yield from restaking on other protocols as well.

#3 Solana comeback?

When FTX crashed, $SOL was on its way to the afterlife.

SBF heavily promoted it, and when he took the Fraudster of the Year award, $SOL lost a ton of value. Few tokens on Solana were low-float high-FDV S(c)AM tokens as well.

But the community kept going. And Solana seems to be making a comeback.

Solana has an active dev community. And the numbers are green on its DeFi protocols.

It seems to have fixed the chain outage issues. It didn’t have any chain outages in Q2 and Q3.

When the total Crypto & DeFi TVLs crashed, Solana TVL increased by 18.52% in Q3. It went from having $770.88 million on June 30th to having $913.66 million on October 1.

It also had several bullish developments in Q3.

- Maple Finance returned to Solana.

- Shopify integrated Solana into their platform.

- Visa added stablecoin settlement on Solana.

- Many DeFi protocols on Solana are growing.

- Membrane Finance introduced the Euro stablecoin on Solana.

- Recognition as a superior-tech for execution engine. (MakerDAO’s founder wanted to create an L1 for Maker using Soalana’s codebase.)

I’m bearish on Layer 1s right now, but Solana could be the exception.

What’s Next?

While looking back is good for learning lessons, real opportunity is in looking forward.

- The Arbitrum Ecosystem. They approved a 50 million $ARB incentive program. It’ll last until January 31, 2024. So, degen money chasing yield will be going over to Arbitrum.

The DAO is voting on which projects should receive the funding. The best strategy is to pay attention to protocols that are going to get incentivized and take a position in them (make sure they fit your investing strategy tho).

- Canto has been pumping recently. It was a Cosmos chain that introduced economic innovations such as

- directing % of the gas fee paid towards smart contract developers. This incentivizes devs to build on Canto.

- Financial primitives such as DEX, lending market, and stablecoins were provided as public goods without any fee.

- Recently they announced that they’re migrating to be a ZK L2 on Ethereum using Polygon CDK. They have also partnered with Fortunafi & Hashnote for their RWA strategy. The Layer 2 and RWA narratives are two powerful narratives. I’ll be closely monitoring them.

- We’ll also monitor the usual suspects: decentralized perps, ETH Layer 2s (Base, Mantal), LSDfi, LRTs (Liquid Restaking Derivatives), GamblFi, Cosmos, Solana, etc.

I might be forgetting some things, but it’s 2 a.m.

On a longer timeframe, I’m looking forward to Ethereum’s Dencun upgrade. It’ll introduce proto-danksharding, an update that’ll make it cheaper for rollups to use Ethereum. Similar to how Shapella upgrade was a catalyst for LSDfi narrative, the Dencun upgrade can be a catalyst for Layer2 projects.

On a larger scale, there’s the geopolitical backdrop of Israel-Hamas conflict. I keep politics out of this newsletter, but I wanted to bring it up because it could affect the markets.

Overall, I see this being a quiet Quarter 4.